Tuesday, January 24, 2017

Important Formulas for Supply

- Fixed Cost: Cost that does not change no matter how much of a good is produced

- Variable cost: Cost that rises or falls depending upon how much is produced. ex: electricity bill.

- TFC + TVC = TC

- AFC + AVC = ATC

- TFC/ Q = AFC

- TVC/ Q = AVC

- TC/ Q = ATC

- AFC x Q = TFC

- AVC x Q = TVC

- marginal cost = new TC - old TC

Q = quantity

TFC = total fixed cost

TVC= total variable cost

TC = total cost

MC = marginal cost

AFC = average fixed cost

AVC = average variable cost

ATC = average total cost

January 20 2017

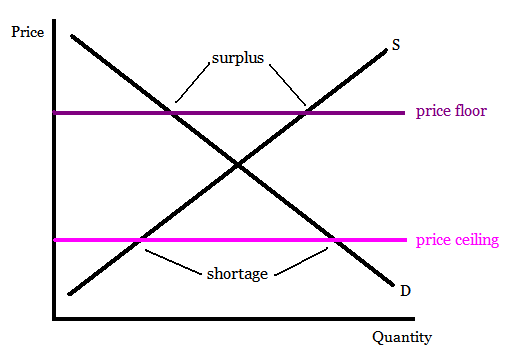

Excess Demand

Excess Demand

Excess demand: quantity demanded is greater than quantity supplied (shortage). Ex: flu shots at Walgreen's

Shortage: consumers can't get quantity of items they desire

Equilibrium: Point at which supply/demand curve intercept

Price ceiling: occurs when government puts a legal limit on how high the price of a product can be. (must be set below the equilibrium mark to be efficient)

Excess supply: quantity supplied is greater than quantity demanded (surplus)

Surplus: when the producers have inventory they can't get rid of.

Price Floor: Lowest legal price a commodity can be sold at. (Used by government to prevent prices from becoming too low) ex: minimum wage.

January 11, 2017

Elasticity of Demand

Elasticity of demand: Measure of how consumers react to a change in price.

Elastic demand

- Demand that is very sensitive to a change in price

- Product is not a necessity

- Always greater than 1

- Available substitutes

- Example: soda, coats, steak

Inelastic demand

- Demand that is not very sensitive to a change in price

- Product is a necessity

- Few/ no substitutes

- Less than one

- Example: gas, insulin

Unitary elastic

- Equal to one (in a perfect society)

Total Revenue: total amount of money a company receives from selling goods and services.

Formula: Price x Quantity

January 3, 2017

Macroeconomics- The study of economy as a whole

Positive economics: claims attempt to describe the world as is. Very descriptive in nature. Fact-based

Normative economics: claims attempt to describe how the world should be. Opinion based.

Needs vs. Wants

Needs: basic requirements for survival

Wants: desires

Scarcity vs. Shortage

Scarcity: fundamental economic problem that all societies face. How to satisfy unlimited wants with limited resources.

Shortage: quantity demand it exceeds quantity supplied.

Goods vs. Services

Goods: tangible (touchable) commodities. Capital/consumer goods. Capital goods are items used in creation of other goods. Consumer goods are goods intended for use by consumer.

Services: work that is performed for someone. ex: entertainment, getting haircut, etc.

Two Types of Efficiency

- Productive- Products are being produced in the least costly way. Any point on the PPC

- Allocative- Products being produced are the ones most desired by society

January 4, 2017

Factors Of Production

- Land: natural resources

- Labor

- Capital (human/ physical) human: when ppl acquire skills and knowledge through experience/education. Physical: money, tools, buildings, machinery etc

- Entrepreneurship: involves risk taking, being inventive/innovative. Takes 3 factors of production to promote the business.

Trade-offs: alternative we sacrifice when we make a decision

Opportunity cost: next best alternative

Guns or butter: trade-offs a country faces when choosing whether to produce more or less of military goods or consumer goods

Thinking at the margins: deciding whether to add/subtract one additional unit of some resource

Efficiency: using resources in such a way to maximize production of goods/services. Increases profits

Under-utilization: opposite of efficiency. Using fewer resources, leads to decreased profits.

Subscribe to:

Comments (Atom)